Between Fiscal Years (FY) 1998 and 2005, the House of Assembly budget for allowances and assistance was overspent by a total of more than $3.2 million but Auditor General John Noseworthy's report on alleged overspending by five current and former members of the provincial legislature accounts for less than half that.

The figures come from a comparison of Noseworthy's reports with the Public Accounts for each fiscal year. The Public Accounts are the official financial statements for the provincial government, audited annually by Noseworthy (right, Photo: CBC) and his predecessor Elizabeth Marshall in accordance with the Financial Administration Act. The Public Accounts are compiled from records maintained by each department and confirmed by the comptroller general, the provincial government official whose office has been issuing cheques on behalf of the House of Assembly since 1999.

The figures come from a comparison of Noseworthy's reports with the Public Accounts for each fiscal year. The Public Accounts are the official financial statements for the provincial government, audited annually by Noseworthy (right, Photo: CBC) and his predecessor Elizabeth Marshall in accordance with the Financial Administration Act. The Public Accounts are compiled from records maintained by each department and confirmed by the comptroller general, the provincial government official whose office has been issuing cheques on behalf of the House of Assembly since 1999.Bond Papers corrected the Auditor General's reporting of dates to coincide with the Public Accounts.

Sudden jumps in individual payments

Figure 1 (above) shows the results of Noseworthy's reports on five current and former legislators. Before 2001, payments over budgeted amounts to individual members of the legislature were relatively small. However, they skyrocket in 2001. One member who allegedly received $12,000 more than budgeted in FY 2000 with one member, allegedly received $118,000 the following year, followed by more than $128,000 in FY 2002 and $198,000 in FY 2003 before the overpayments suddenly stopped.

Figure 1 (above) shows the results of Noseworthy's reports on five current and former legislators. Before 2001, payments over budgeted amounts to individual members of the legislature were relatively small. However, they skyrocket in 2001. One member who allegedly received $12,000 more than budgeted in FY 2000 with one member, allegedly received $118,000 the following year, followed by more than $128,000 in FY 2002 and $198,000 in FY 2003 before the overpayments suddenly stopped.Another member, defeated in the 2003 general election, allegedly received approximately $9,900 in FY 2000, $41,800 in FY 2001 but more than $130,000 in FY 2003.

While three of the five members received no overpayments after FY 2003, two current members of the legislature received overpayments in FY 2004 and FY 2005.

The Public Accounts show that the House of Assembly's allowances and assistance budget - the line item that covers constituency allowances - was overspent in each year from FY 1998 to FY 2005.

Bulk of unexplained overspending occurred after April 2004

Figure 2 (above) shows a comparison of the total overspending on the allowances budget each year (red line) with the total overspending contained in the Auditor General's reports on alleged overspending by five current and former members (yellow line).

Figure 2 (above) shows a comparison of the total overspending on the allowances budget each year (red line) with the total overspending contained in the Auditor General's reports on alleged overspending by five current and former members (yellow line).Except for two fiscal years, the alleged overpayments to individual members is far below the total overspending on the budget line item. Overspending in FY 1999, for example, totaled more than $529,000 but the Auditor General's reports only account for approximately $78,000.

Similarly, alleged payments to two members in FY 2004 and FY 2005 total slightly over $200,000. Total overspending reported in the Public Accounts for those same years totals more than $1.0 million, about half of the overspending still unexplained by the Auditor General after completing two separate reviews of overspending. Coupled with the questioned suppliers' payments (see below), the bulk of the alleged overspending and questionable payments occurred after 2004.

When he announced results of his first review of spending by Byrne, Noseworthy said that changes to the administrative rules in 2004 prevented overspending after that date.

No explanations; AG and Finance Minister get dates wrong

AG Noseworthy stated recently that his reviews of overspending are completed. His next public report will examine how members of the legislature spent their allowances beginning in 1989. He has not explained how he believes certain individuals received overpayments, nor has he explained the total overspending on allowances.

In releasing his latest report on individual overpayments, Noseworthy did note that the individual overpayments accelerated after the Auditor General's office was barred from reviewing the legislature's accounts, supposedly in FY 2000. In recent media interviews, finance minister Loyola Sullivan, a member of the legislature's internal economy commission since 2002, stated he regretted making the decision in FY 2000.

However, the decision to block the Auditor General's review was taken in 2002, not 2000. Sullivan (left) was a member of the IEC when the decision to block the Auditor general was actually taken. Changes to the Internal Economy Commission Act in 1999 and 2000 gave the IEC the power, among other things, to determine who would audit the legislature's books.

However, the decision to block the Auditor General's review was taken in 2002, not 2000. Sullivan (left) was a member of the IEC when the decision to block the Auditor general was actually taken. Changes to the Internal Economy Commission Act in 1999 and 2000 gave the IEC the power, among other things, to determine who would audit the legislature's books.In April 2004, the Internal Economy Commission removed the bar on the auditor general but stipulated the audits would be from April 2004 forward. That restriction was only removed after Noseworthy's allegation in June 2006 when he was sent back to re-do his original work.

The Auditor General has been legally able to audit the House of Assembly accounts for all but a two year period. Under the Financial Administration Act, the AG cannot legally be barred from reviewing the comptroller general's payment records. Those records form the basis of the Public Accounts and include details of the overspending from FY 1998 to FY 2005 Noseworthy has thus far not discussed.

Neither Sullivan nor Noseworthy has explained the discrepancy in their version of events or why the auditor general's office did not comment on the consistent overspending of the allowances account between 1998 and 2005.

Suppliers' payments don't fill in gaps in story

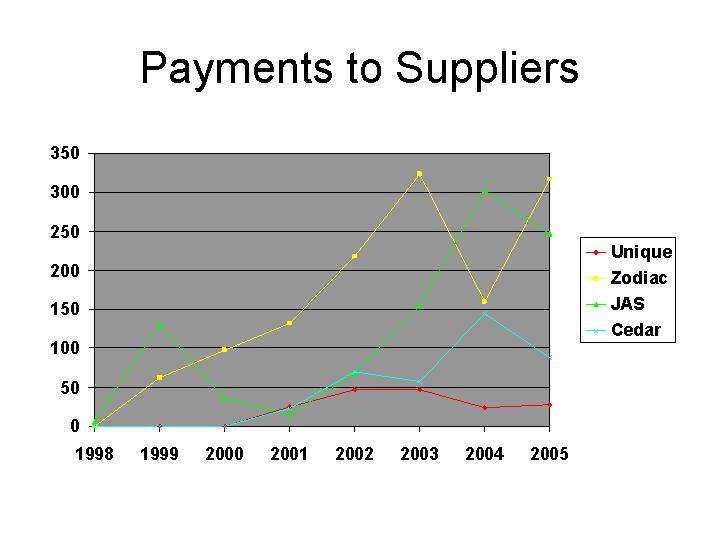

Noseworthy has also questioned payments to four suppliers made by the legislature between 1998 and 2005.

Noseworthy has also questioned payments to four suppliers made by the legislature between 1998 and 2005.Figure 3 (above) compares the payments, based on the Auditor General's reports

However, while Noseworthy has alleged some goods purchased from the companies was never received, he has not been able to demonstrate this conclusively. In his initial report, Noseworthy claimed his office had been unable to confirm that items - such as expensive but poorly made signet rings - had been delivered. Within an hour of Noseworthy's news conference last summer, several rings turned up.

As well, Noseworthy has only attributed only a small portion the $2.6 million apparently paid to the companies to the five individual members of the House of Assembly. Most notably, though, the payments to the companies made in FY 2004 and FY 2005 total more than the entire overspending for the period as reported in the Public Accounts.

AG admits definition of "inappropriate" will be highly subjective

Rather than provide a complete explanation of overspending in the House of Assembly, the Auditor General will now focus his attention on how members of the legislature spent money allocated for constituency expenses regardless of whether the members overspent their accounts.

This is actually outside the mandate given him by cabinet in July 2006, while a detailed accounting of the overspending between 1998 and 2005 would be exactly described in his charge to conduct "detailed audits" for the period.

Attention will be focused, some believe, on former finance minister Paul Dicks who allegedly purchased wine and artwork from his constituency budget. According to some reports, Noseworthy and his then-boss Elizabeth Marshall were reviewing Dicks' accounts when they were barred from the legislature books in 2002.

Noseworthy has indicated this portion of his review - which may or may not be completed before the next general election - will examine spending dating back to 1989. Noseworthy's hunt for overspending by individual members found nothing before 1997. Bond Papers predicted as much in June.

At the same time, some members of the legislature, including Liberal opposition leader Gerry Reid and Speaker Harvey Hodder, the Progressive Conservative member of the legislature for Waterford Valley have admitted to providing donations to groups in their districts and purchasing personal advertising from their constituency allowances.

In an interview with CBC television's Debbie Cooper, Noseworthy said he will be basing his assessment of "appropriate" spending by compiling a database of what members were spending allowances on. He told Cooper his definition of "appropriate" would be subjective.